Surveys

DJC.COM

December 7, 2007

Hot Eastside office market won’t get red hot

Broderick Group

Sweeney

|

The Eastside office market has felt red hot over the past six months, especially in comparison to the collapse in the markets of 2000 and 2001. The recovery is now complete. So, what is driving that market and where is it headed in the next three years?

POSITIVE FACTORS:

• Microsoft has leased more than 2.4 million square feet over the last 18 months.

• Equity Office Properties sold its properties to Beacon and Archon. The new owners of the former EOP portfolio have brought Bay Area pricing to Seattle, in particular to the Eastside. Their rate adjustments, coupled with Microsoft’s announcements, have been enough to increase rental rates more than 20 percent for the year.

• Large tech tenant lease signings have garnered significant media attention and created the impression that the office market is overheated. Highlights include Google taking 195,000 square feet at Lakeview Plaza in Kirkland, Yahoo signing on for 115,000 square feet at One Twelfth @ Twelfth in the Bellevue CBD, and Expedia leasing 346,000 square feet at Tower 333 in the Bellevue CBD. Additional leases by predominantly high-tech companies totaling in excess of 100,000 square feet are soon to be announced.

THE NEGATIVE FACTOR:

The national economy is causing a drag. While the Eastside office market is certainly strong, the weakness brought on by the national economy is affecting the local market. In particular, mortgage companies and other related financial service companies have been slowly and quietly vacating or subleasing spaces, creating an abundance of 5,000- to 15,000-square-foot spaces. The greater Seattle-area office market continues to enjoy strong job growth and its accompanying demand for space. However, we are not insulated from national concerns, and the conservatism of national companies in our area is keeping this office market from becoming red hot.

Vacancy rates

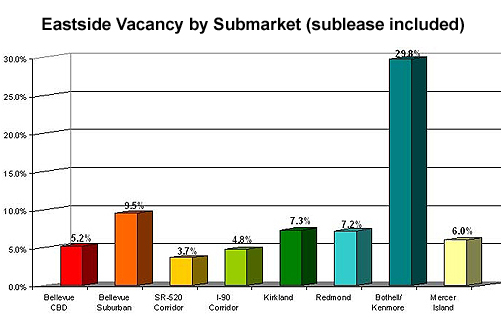

The vacancy rate for Eastside office buildings (Class A and B, including subleases) is 8.9 percent — not red hot but under the 10 percent rate that has historically accommodated rental rate growth. If you take out the Bothell submarket, and its 30 percent vacancy rate, the Eastside office market is an even more healthy 6 percent.

Eastside investment/sales

Cap rates for the Seattle-area office market overall have been higher this year, averaging 6.4 percent, compared to the same period last year when they averaged 5.9 percent. Lack of good-quality product has been the norm during the past two years (with the exception of the EOP portfolio).

Recently, there has been a slight increase in available investment properties located in or near downtown Bellevue, including Washington Mutual Plaza, the 200 Building, Commons Professional Center, Brookside Office Park and I-405 Corporate Center. These buildings have not yet sold, but will shortly.

Sellers have realized that unbelievably low cap rates may not last, contributing to the increase in inventory. Buyers are still aggressive and continue to bet on future rental rate increases.

Many believe that buyers are currently underwriting lease assumptions far too aggressively. Generally speaking, it is better to be a seller than a buyer in the Eastside office market at this time.

Rental rates/leasing

Average rents have grown approximately 20 percent, year to date. This is a continuation of the recovery from the rental rate fallout during 2001 and 2002. Never before has the market seen such activity from large users. This has fueled rent increases, taken large blocks of space off the market and accelerated contemplated development.

Despite the headline-sized deals, interest from small- to medium-sized companies has, at best, been moderate. Nevertheless, as long as vacancy rates remain less than 10 percent and given the expensive land and construction costs to bring new buildings to market ($400-plus per square foot in Bellevue), upward pressure on rental rates will continue for the next year.

The 2008 office market

Vacancy rates will increase slightly to about 9 percent by the end of 2008. The Eastside market will deliver 3.1 million square feet of new construction in 2008, its second highest total ever. Two million square feet of this new construction is already leased, and demand is strong for “close-in” new construction.

Expect space givebacks and continued conservatism from national firms, particularly the financial services sector, to result in some slowing demand. Due to Microsoft’s significant commitment to much of the 2008 deliveries, it will remain a landlord’s market, with healthy 10 percent rental rate increases anticipated.

The 2009 office market

Net absorption (new and existing net space leased) will slow, but with a reduced amount of new construction (1 million square feet) coming to market, vacancy rates will again tread water, staying in the 9 percent range. We expect a 5 percent growth in rental rates.

Microsoft is the obvious driver of the Eastside economy; the firm will occupy roughly 4 million square feet of leased space in the Eastside office market by 2009, which is 12.5 percent of the entire inventory. This is in addition to the approximately 9 million square feet it now owns.

Microsoft represents more than 25 percent of all Class A and B owned and leased office space on the Eastside. These numbers do not begin to factor the many companies that service Microsoft. When considered in total, their percentage of space alone, not to mention their multiplier effect in creating other demand for space on the Eastside is staggering.

So if we all want to know what will happen to the Eastside market, it would be better to be a Microsoft stock analyst than a real estate broker. What we do know is much of the 1.05 million square feet of space the firm leased in 2006 is distributed throughout smaller spaces with shorter-term leases in buildings it would not typically occupy. With the completion of current construction on campus, expect Microsoft to do some retreating in 2009 and 2010, which will definitely let some air out of the Eastside office market.

The 2010 office market

Unlike the savings-and-loan crisis in the late 1980s that resulted in an oversupply of space, and unlike the dot-com bust of 2000 where oversupply was created by tenant givebacks, we hope for a soft landing in 2010. We do, however, expect a definite downturn in this current up cycle, as the strong Northwest economy may be dragged down by the national economy and potential Microsoft retreats to its Redmond campus create unexpected vacancies.

Images courtesy of the Broderick Group Submarket vacancies on the Eastside are the highest in the Bothell/Kenmore area. |

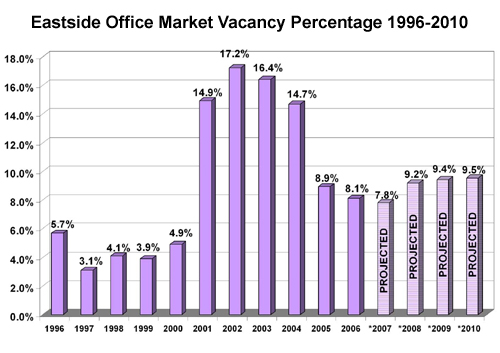

Eastside office vacancies are leveling off after the dot-com bust. |

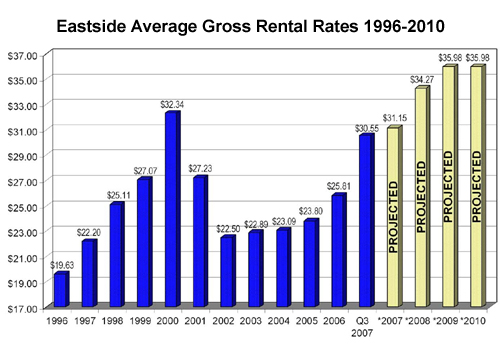

Eastside office rental rates are projected to reach all-time highs next year. |

Paul Sweeney is a cofounder and principal of the Broderick Group, a commercial brokerage firm with Seattle and Bellevue offices specializing in the sale and leasing of office and high-tech properties. Sweeney has 21 years of experience in office leasing and sales on the Eastside.

Other Stories:

- Commercial real estate continues its strength

- Use cost segregation to cut Uncle Sam’s bite

- Too many condos in Seattle? Think again

- An urban village emerges on Seattle’s First Hill

- Pros and cons of the Industrial Jobs Initiative

- What’s next for Seattle’s CBD office market?

- Developing retail? Here are some things to know

- Downtown becomes too pricey for disabled homeless

- Workforce housing shortage is a ‘silent epidemic’

- Now is the time for apartments — but beware!

- Will good times continue for our market?

- Full speed ahead as CBA turns 30

- CBA Insights speaker profile: Dennis Wilde

- CBA Insights speaker profile: John Parker

- CBA Insights speaker profile: Linda Berman

- Retail evolves in mixed-use projects

Copyright ©2009 Seattle Daily Journal and DJC.COM.

Comments? Questions? Contact us.