Surveys

DJC.COM

December 11, 2008

Seattle’s office market: No more high-fiving

Grubb & Ellis

Hill

|

Last year at this time, commercial real estate professionals were high-fiving one another on a banner year for the city of Seattle: Low vacancies, high lease rates and blockbuster sales volumes made 2007 one of the best years on record for our industry. Most players in the market — including Grubb & Ellis — expected the market to continue improving in 2008, albeit more moderately. Supply would increase just enough to meet surging demand, the thinking went, and the market would not trend downward until late 2009 or early 2010, fulfilling Seattle’s historical 10-year real-estate cycle.

These predictions, of course, all occurred when interest rates were 5 percent, five large independent investment banks fueled the capital markets, Seattle was home to the nation’s largest savings and thrift, nobody had heard of collateralized debt obligations, and commercial mortgage-backed securities were the future of the industry. In other words, the world looked much different a year ago.

|

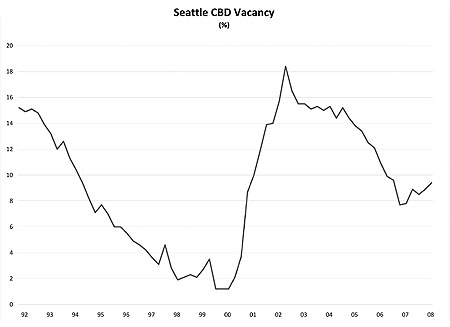

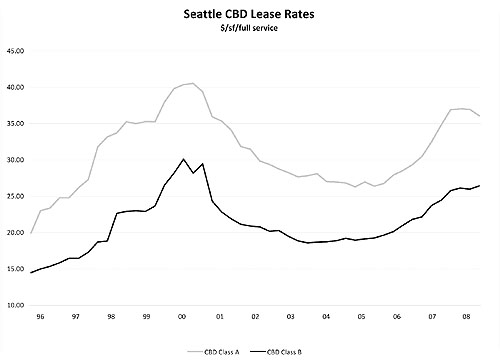

Seattle’s vacancy rate increased 90 basis points, from 8.5 percent to 9.4 percent, through the first three quarters of 2008. Class A rates — after increasing 25 percent during 2007 — remained essentially flat during 2008, falling 2 percent to $35.07 on a full-service basis. Net absorption, the primary measure of demand in the commercial market, was 62,493 square feet in 2008, a sharp drop from the same time in 2007, when it was 613,619. All of these numbers tell the same story: The Seattle office market has begun to soften earlier and more sharply than widely expected.

Supply

Available space increased markedly during 2008, as several new buildings hit the market and many tenants chose to sublet a portion of their existing leases. Available sublease space increased 65 percent, to 985,787 square feet, through the first three quarters of the year. Major sublease blocks added to the market this past year included: F5 (40,000 square feet), Safeco (70,000 square feet) and Starbucks (226,840 square feet).

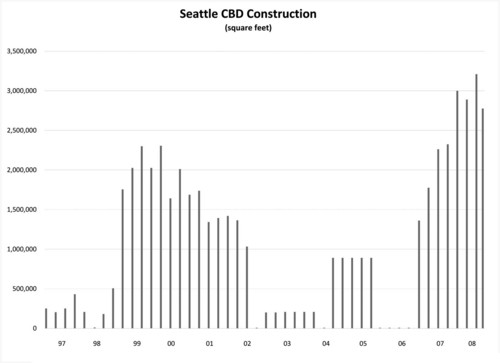

Developers, ostensibly chastened by the dot-com bust when many were left in the lurch by a sudden market shift, claim to have avoided the mistakes of the recent past. The numbers, however, suggest otherwise. More space is under construction in the Seattle CBD — 2.8 million square feet across 10 projects — than at any point during the past 20 years, with the notable exception of earlier this year, when total projects under construction surpassed 3 million square feet. Some of those projects have subsequently been completed.

These numbers significantly exceed the dot-com boom high of 2.3 million square feet, reached in June of 2000. As it stands today, moreover, none of the projects have pre-leased any space.

Demand

The economic engine of the Puget Sound, fueled in recent years by job growth in the construction and financial services industries, began sputtering in the second quarter of 2008, when only 1,100 net jobs were created across the region — a lackluster 0.2 percent annualized growth rate. According to the Puget Sound Economic Forecaster, four-fifths of the current slowdown can be pinned on construction.

Only 6,400 jobs will be created during 2009, the report continues, meaning layoffs will roughly match any new hires. The revised November report from the Washington State Economic and Revenue Forecast Council, our state government’s official economic forecast, predicts a statewide decrease in nonfarm payroll employment of 21,400 jobs in the upcoming year, a 0.7 percent decline.

With local big hitters like Starbucks, Alaska Air and F5 cutting costs — and others, like Washington Mutual and Safeco, being subsumed by outside firms — no clear white knight sits on the horizon. Even Microsoft, which leased more than 1.8 million square feet in 2007, may finally be slowing down. In October, the company announced $500 million in targeted cost reductions, specifically identifying facilities and data centers.

Local government, oft-cited as another possible downtown savior, faces looming deficits: Seattle ($19 million), King County ($93 million) and the state ($5.1 billion).

The bottom line: Few local tenants are looking to expand into new space, and many are actually looking to contract.

Equilibrium

Basic math tells the rest of the story. For office demand to keep up with supply, 11,100 white-collar jobs would need to be created in Seattle during 2009 (using the 250 square feet per office worker rule of thumb). This, quite simply, will not happen.

Our models, based on the job trends and construction pipeline detailed above, project that vacancy will increase to somewhere between 14 percent and 15 percent in Seattle by the end of 2009. Lease rates, predictably, will fall, as tenants find themselves faced with multiple moving options and a buffet of concessions. Average Seattle CBD Class A lease rates may dip back down below $30 per square foot, levels last seen at the end of 2006.

These trends will not reverse until the economy, as a whole, turns the corner — an event most economists now predict will occur in early 2010.

The big picture

As a veteran of this market for 25 years, I have seen the delirious highs of the dot-com boom — CBD vacancy was 1.2 percent in March of 2000 — and the miserable lows brought on by the Resolution Trust Corp., when vacancy was 16 percent in June of 1992. Our current situation, I am happy to report, bears little resemblance to either of the past two market swings.

The run-up to our present market, roughly 2003 through 2007, was shorter (five years) and shallower (10.7 percentage points drop in vacancy from peak to trough) than the last bull market in the 1990s (eight years and 14 percentage points drop). Moderation begets more moderation; a restrained high yields a less harmful low.

Whereas the aftermath of the dot-com boom produced 18 percent downtown vacancy, we expect rates to reach only 14 percent to 15 percent this time around. High? Yes. Devastating? Not a chance.

The only market participants likely to falter are those with high debt service payments, little cash flow, or both (read General Growth Properties). As last month’s article in the Daily Journal of Commerce, “Seattle commercial real estate players: ‘We’re not immune,” pointed out, most local developers are well capitalized and well positioned for the market rebound in 2010.

Stronger and wiser

Let’s be frank, the state of the Seattle office market is weak and getting weaker. Yes, we are in a recession. And no, Seattle is not immune. If anything, the past year has taught us just how truly global, interconnected — and fallible — the Puget Sound economy is.

As with past downturns, however, Seattle will emerge stronger and wiser. One of the nation’s most educated, innovative, entrepreneurial and diverse cities, Seattle will always be a hotbed of business development.

Looking further out into the future, vacancy rates will stabilize during 2010 and resume tightening in early 2011, due to a rebounding economy and constrained new supply.

Until then, I suggest we keep this downturn in proper perspective. The sky is not falling and the end-of-days is not at hand. Bust follows boom and debt must eventually be unwound; this is the nature of our industry. Most market players will emerge bruised, but intact and, hopefully, a little wiser for the next go-around.

Craig Hill has been involved in the local commercial real estate market for more than 30 years and is a senior vice president at the Seattle offices of Grubb & Ellis.

Other Stories:

- CBA speakers take on the economy

- A green future for savvy developers

- Making green design deliver ROI, not just LEED

- Market District evolves as a walkable neighborhood

- Mixed-use projects can pay off handsomely

- Local retailers will fare better than others

- Suburban hubs will draw tomorrow’s renters

- Industrial market hums along, but don’t hold your breath

- CBA ready to mint a new breed of green brokers

- Weathering the storm

- Young guns take their shot at the market

- David A. Sabey

Sabey Corp. - Sean G. Hyatt

Trammell Crow Residential - Lynn Michaelis

Weyerhaeuser Co. - Dan Ivanoff

Schnitzer West - Commercial real estate prepares for the future

- The pitfalls of renting out condo projects

Copyright ©2009 Seattle Daily Journal and DJC.COM.

Comments? Questions? Contact us.