Surveys

DJC.COM

December 15, 2005

How rising interest rates will affect real estate

Special to the Journal

Makar

|

Fosseen

|

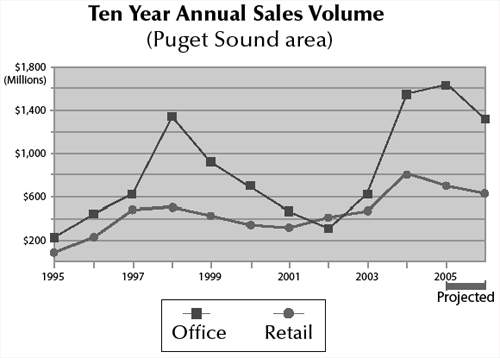

In 2005, we saw record high volumes in investment sales and real estate financings, both in the national and local markets. The following details investment sales over $10 million in the retail and office arenas in the Puget Sound.

The retail market

The retail market continued to be a favored investment type for both institutional and private investors. Total sales for retail properties dropped from 2004, however this was due to lack of product, not lack of demand. Year-to-date, 20 shopping centers have traded hands for a total volume of $542.1 million, averaging $220 per square foot. Cap rates ranged from 6 percent to 6.75 percent for smaller strip centers, to 6 percent to 6.45 percent for anchored neighborhood and power centers. For several, opportunity sales capitalization rates were not even a consideration in the pricing.

The sales were priced based on their values after renovations and expansions to be completed by the new owner. Examples of this were the regional centers: Everett Mall and the former SeaTac Mall (rechristened The Commons at Federal Way).

While the Puget Sound retail market has remained strong through this real estate recession with vacancy rates never above 4.5 percent, and current vacancy at 1.9 percent, rents have not grown appreciably in all property types. Institutional purchasers are reportedly targeting unleveraged internal rates of return in the 7.5 percent to 8.5 percent range for core assets, with targets of low double digits with market growth and property upgrades.

The office market

The Seattle office arena gained favor with institutional investors in 2005, with most believing it will grow faster than the rest of the country in 2006.

So far in 2005, 32 office buildings traded totaling over $1.3 billion in value. Prices per square foot also skyrocketed in 2005. An eye-popping example was Civica in Bellevue selling for $458 per square foot, a figure normally achieved only in major markets like New York and San Francisco. Also, 5th & Pine in downtown Seattle traded for $387 per square foot.

The volume of sales and the apparent increases in values were not driven by underlying strength in the market, but by the perceived growth in the coming years. While occupancies have increased, other than in the Bellevue CBD, they are still not up to the level that is assumed by buyers when they make the purchases (i.e. most buyers like a 5 percent vacancy rate).

Interest rates effects

The drivers of this run up in real estate values have been much written about and documented. Compare real estate to other investments: stocks have preformed poorly for five years; until recently, short-term investments were under 2 percent; and bonds had the twin features of both low yields and increasing skepticism about the underlying veracity of the credit ratings of the companies.

Further, during 2004 and early 2005, buyers could still get positive leverage even when buying properties at historically low cap rates.

During the first three quarters of 2005, buyers who wanted loans that were 75 percent to 80 percent of purchase price, could borrow in the 5 percent to 5.25 percent range, often with interest only for several years. Institutional borrowers, such as pension funds and REITs, could put on debt at say 50 percent of the purchase price and get pricing under 5 percent with perhaps the whole 10 years interest only. This leverage could easily increase the initial cash return from 5.5-6 percent to 7-9 percent, depending on the amount of leverage used.

However, for the last quarter of 2005, and we expect for all of 2006, this leverage boost will be lower or nonexistent since interest rates have gone up and are forecasted to go higher.

The 30-day LIBOR (London Interbank Offered Rate) has nearly doubled since January, and the yield on the 10-year treasury has risen to about 4.5 percent since this summer — driving mortgage rates to the 5.5-6 percent range. The average forecast from 19 top investment banks and research firms estimates the 10-year treasury to be 4.93 percent in mid-2006 and 4.84 percent by year-end 2006. The same group forecasts short-term rates to rise by a similar 40 to 50 basis points.

While we are not predicting that cap rates will rise in direct proportion to interest rates, nor that they will they move immediately, this increase in rates should have a dampening effect on prices and volume for certain property types. The increase in rates will be noticeable, but will not be a huge increase and the impact will be tempered.

A simplistic way to think about the expectations for values is to imagine there are two primary drivers of value: the underlying health of the market and interest rates. In the best of all worlds, we would have a strong market and low rates. This may have happened for a few months in 1998-1999, but it is rare.

The worst of all worlds was the early 1990s, when we had poor fundamentals and high rates; no one wants to see that again.

For the past three years, we've had a mixture of a poor market and low rates, with strong resulting values.

We are entering another mixed period with strong fundamentals but higher rates. The most recent similar period was 1995-2000. If the market replicates the experience of that period, most investors will be happy and buyers still eager. Values should hold, even if sales volumes diminish.

The healthy fundamentals should keep the Puget Sound area on the screens of both national and international institutional investors and, unless these investors start to increase their internal rate of return expectations, there should not be a fall off in their prices or cap rates. While these institutional buyers used leverage to improve their yields, they were not driven by leverage and will now simply buy properties and hold them debt free if debt is too expensive.

The private capital that seeks 75 percent to 80 percent leverage, however, is another matter. Due to debt service coverage constraints, they will no longer be able to achieve desired loan amounts if they buy at cap rates a full percent below long-term mortgage rates. Also, a 1 percent increase in interest rates can result in a 3 percent decrease in cash-on-cash returns for these buyers and investors. Thus it seems reasonable to expect that Class B and C properties, and smaller properties, which typically trade between private owners, will see lower prices in 2006. Also, more failed sales will result due to the inability to meet financing requirements, and re-trading or re-pricing will become more common.

Next year looks very promising, as the healthy economy may permit the optimistic assumptions made by buyers for the past few years to start coming true. For quality Class A product, if sales volume drops off, it will probably be due to lack of product, not falling values.

Institutional buyers will continue to flock to the area paying top dollar, but owners of smaller and lower quality properties may find it is no longer quite the seller's market it has been.

Our advice to sellers is to not panic, but sell sooner than later to minimize interest rate risk during 2006.

Image courtesy CB Richard Ellis

Sales volumes for Puget Sound area office and retail space are beginning to taper off.

|

Michal Makar is managing director of the Seattle office of CBRE-Melody, a commercial mortgage-banking subsidiary of CB Richard Ellis. Don Fosseen is first vice president of the Seattle Investment Team for CB Richard Ellis.

Other Stories:

- Richard Lee

- 8 questions office tenants should be asking

- It's time for housing in downtown Olympia

- Visionary property owners try some new tools

- Pullman developer's mantra: Learn from your mistakes

- Making today's mixed-use projects work

- How do lease options work?

- Resurrecting the Technology Corridor

- Will hurricanes puff up insurance rates here?

- How Trammell Crow hit the real estate jackpot

- Lifestyle centers: A return to Main Street USA?

- Is it safe to jump back into the condo market?

- CBA is bullish on the commercial market

- Arthur Rubinfeld

- Bill Morton

- Here's what's in store for retail properties

Copyright ©2009 Seattle Daily Journal and DJC.COM.

Comments? Questions? Contact us.