|

Subscribe / Renew |

|

|

Contact Us |

|

| ► Subscribe to our Free Weekly Newsletter | |

Construction Bids

| home | Welcome, sign in or click here to subscribe. | login |

| |

|

October 29, 2015

Cline

|

Stadelman

|

A 2010 legislative tax law change in Washington state regarding apportionment of certain revenue streams affects in-state companies as well as those that are out-of-state but operating in Washington. It isn’t an extension of the old method, but a dramatic change that takes effort to understand.

Standing to benefit are taxpayers operating within Washington that derive income from in-state and out-of-state sources, which may vary based on where the benefit is received contractually or practically. On the flip side, taxpayers operating out-of-state that derive income from Washington sources, which again may vary based on where the customer’s benefit is received, may owe incremental business and occupation taxes.

This new legislation isn’t entirely unique to Washington state. More and more states are adapting to collect tax from businesses that have no physical location in the state yet derive economic gains from the state’s economy. Its reach stretches to companies working on foreign land but doing business in Washington. The law also helps create jobs by attracting companies to the state with tax breaks.

Far more architecture and engineering firms will be impacted — particularly those outside of Washington — and many of them will continue to use the old method due to complexity, lack of understanding or inertia.

Many in-state A&E firms may benefit financially through a review — some companies derive multi-million-dollar benefits — depending on facts and circumstances. Likewise, out-of-state A&E firms may get additional tax bills due to Washington on account of this legislation.

Regardless, this is a great opportunity for many taxpayers who are incorrectly reporting to clean up shop, and we’re finding that many Washington companies end up with refunds.

General guidelines

Washington’s B&O tax is a tax on gross receipts allocated and/or apportioned to the state. A company is deemed to have substantial nexus in the state if it has:

• More than $250,000 of Washington receipts

• More than $50,000 of Washington property

• More than $50,000 of Washington payroll

• At least 25 percent of total receipts, payroll or property in Washington

While some A&E firms might have other revenue streams that aren’t relevant to this discussion, most are taxed at the general service and other rate, which is 1.5 percent. And remember, the business doesn’t need to have a physical office in the state.

Expanding parameters

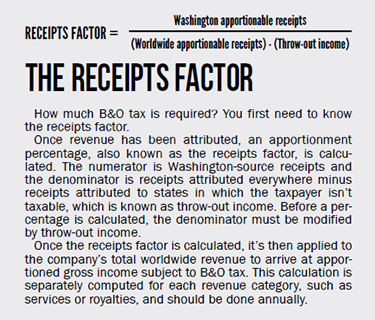

Revenue is allocated under a series of steps. The first step provides for the sourcing of service receipts — or where the customer received the benefit of services rendered — which is commonly referred to as “reasonably determining.”

Most taxpayers are expected to reasonably determine revenue through proportionally attributing revenue amongst the states where customers receive the benefit of services rendered, according to Rule 19402. The rule also states if a taxpayer performs services for the benefit of a third party, the term “customer” means the third-party beneficiary.

Realizing the ambiguity involved in determining where the customer received the benefit, the Department of Revenue expanded its parameters. If the service relates to real property, then the benefit is received where the real property is located. Here’s a nonexclusive list of services that relate to real property:

• Architectural

• Surveying

• Janitorial

• Security

• Appraisals

• Real estate brokers

Engineering firms may have services related to real property or tangible personal property (TPP). If the service relates to TPP, then the benefit is received where the place of principal use of the TPP occurs. If the TPP will be created or delivered in the future, the principal place of use is where it’s expected to be used or delivered.

Window of opportunity

The statute of limitations for filing refund claims and assessments is four years plus the current, and the statute falls off at the end of this calendar year. There are only a few months left to review the B&O tax methodology for the 2011 tax year and to request a refund if there’s an overpayment under the new rules.

The new rules are complex and taxpayers should check if they’re in compliance. If the result has a high price tag, then investigate practical solutions to achieve a better tax outcome. If there’s an overpayment, then request a refund from the state. This is where a tax advisor might be able to help navigate the many hidden elements to the regulations and take a deeper look so you can increase your state tax savings and reduce exposure while working to put your books in order for a potential excise tax audit.

Adam Cline has provided state and local tax consulting services since 2005. He assists clients with Washington state tax matters and multi-state income/franchise and sales/use tax matters.

Karina Stadelman has practiced public accounting since 1999. She provides business consulting, tax planning and tax compliance services with a focus on professional services firms and the real estate and hospitality industries.

Other Stories: