|

Subscribe / Renew |

|

|

Contact Us |

|

| ► Subscribe to our Free Weekly Newsletter | |

Construction Bids

| home | Welcome, sign in or click here to subscribe. | login |

| |

|

December 13, 2012

Thompson

|

Many building owners already understand the significant benefits associated with performing a cost segregation study, but they may not be aware of the other benefits available to them. Before getting to these, let’s review what cost segregation is.

Cost segregation is a tax-deferral strategy used by many building owners that can provide significant benefits. The goal is to maximize depreciation deductions and increase cash flow by identifying building assets with shorter lives than the building itself, allowing the owner to enjoy substantially faster depreciation on those assets. For example, carpeting may have a life span of five years instead of the building’s 39 years.

Energy incentives

Many building owners that perform a cost segregation study are unaware that they have left dollars on the table and could have taken energy-efficient building deductions but didn’t — simply because they didn’t realize the improvements they had already made were qualified.

Internal Revenue Code Section 179D allows a deduction of up to $1.80 per square foot for energy-efficient components such as lighting, HVAC and the building envelope. The level of energy-efficiency required for the deduction is compared to a baseline standard issued in 2001. Over the past decade, building codes have become much more stringent, often requiring builders to use energy-efficient components and methods (as compared to 2001 building codes).

This deduction is a great benefit for building owners and tenants, but what if you don’t own the building?

If you’re the primary designer of the lighting or HVAC components or the building envelope for a government-owned building, you may be eligible to claim the deduction even though you are not the building owner. Because the government doesn’t pay tax, the energy-efficiency deduction may be available to the primary designer(s) of government-owned facilities, including the architect, engineer, general contractor or other contractors who provided the technical specifications for installation of the energy-efficient components for the facilities.

But what if the construction was completed in previous years and your tax returns have already been filed? Up until 2011 the deduction was required to be taken in the year the qualified property was placed in service. However, the IRS recently issued guidance that provides the option to take the deductions for qualified energy-efficient components as far back as 2006 without amending tax returns. This option is not available to designers of energy components for government-owned facilities; they must claim the allocated deduction on their current year return or amended return in order to take advantage of the benefit.

In addition to the energy deductions, there is a 30 percent tax credit available for installing energy-generating property, including solar, fuel cell and wind devices. In many cases the installation of energy property coincides with the installation of energy-efficient building components related to the deduction.

It’s not uncommon to see energy property undervalued for tax purposes. In many instances a taxpayer will consider the cost of the equipment and installation as “energy property.”

There can be significant value outside of these costs directly related to the support of the energy property that can be easily overlooked. Items such as reinforcement of the original structure to support the energy property may also be considered energy property rather than buildings.

Similar to a cost segregation study, energy studies aim to maximize the value of the energy property through the identification and documentation of the components, improvements and systems supporting the energy property.

New regulations

The IRS this year issued new tangible property regulations, which resulted in the most significant tax change since 1986. As part of these new regulations, taxpayers now have the ability to recognize a gain or loss on dispositions of structural components of a building. For example, assume a taxpayer replaces an HVAC system after 15 years of service. Under the old rules, the taxpayer would continue depreciating the system over the life of the building (typically 39 years for commercial property) and start depreciating the new system (typically over 39 years from the in-service date).

The new tangible property regulations allow the taxpayer to dispose of structural components that are no longer in service and, in many cases, recognize a loss upon the disposition.

The challenge for property owners and tax professionals is how to determine the value of the disposed property, especially if the structural component is part of a larger asset, such as a building. There are a couple of different ways to approach valuing structural components.

The first approach is to segregate the building systems as part of a cost segregation study when the property is constructed or purchased. This approach allows for easy asset identification for determining the amount of gain or loss to recognize upon component disposition.

The second and most likely approach is to carve out the component from the building at the date of disposition. In most circumstances this will entail determining the value of the structural component subject to disposition and recalculating the depreciation on the building and disposed structural component and filing the proper tax form to claim the gain or loss on the disposition.

The rules surrounding cost segregation, energy incentives and tangible property regulations are very complex. It’s best to consult a cost segregation professional or your tax advisor with any questions.

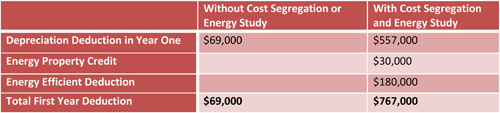

| The benefits of claiming energy incentives |

|

Assume a 100,000-square-foot commercial building was constructed in 2007 and improved in June 2012. The total cost of the 2012 improvement was $5 million, including $100,000 for solar panels. The table illustrates the potential benefits of a cost segregation study on the improvements, coupled with an energy-efficiency study. Based on these numbers it’s pretty evident that doing a cost segregation study and claiming the energy incentives make sense for building owners. What isn’t provided in the table is the potential loss that could be recognized as a result of the dispositions from improving an existing building. To put this into perspective, assume the building was placed into service five years ago at a cost of $5 million, of which $3 million was related to interior structural components. Over that time, the owner would have recovered approximately $600,000 through depreciation deductions (assuming no cost segregation study was completed). As part of the remodel in 2012, all of the original interior structural components were removed. The potential loss as a result of the disposition would be approximately $2.65 million ($3 million less the amount of depreciation taken over five years associated with the interior structural components).

|

Jason Thompson, CPA, leads the cost segregation practice for Washington state and the commercial building energy incentive practice for Moss Adams LLP.

Other Stories: